Ganfeng Lithium: I Don’t See It Improving

Summary

- Lithium supply is abundant, and high prices will not last due to increased production capabilities, leading to eventual price stabilization.

- Ganfeng Lithium’s stock price has dropped from $6.47 to $2.42 in two years, reflecting my earlier bearish stance.

- Ganfeng’s profitability is heavily dependent on lithium prices, which, I believe, will not see a significant long-term rise.

- Investment in lithium is no longer attractive; the market has matured, and future price swings are unlikely to be as dramatic.

xeni4ka

I have, at least, been consistent about lithium

Another advantage is that so far I’ve been right about lithium too. Ever since we all started to get excited about lithium – that essential element for EV batteries and all that – I’ve been pointing out something about these sorts of metals markets. There’s a lot more out there than anyone seems to think.

We therefore never do face a shortage of the actual element we’re after. Sure, we can face current shortage, demand today is higher than supply today. The other description of that is that we just don’t have enough people digging whatever it is up at this time. So, when more people go digging then that current imbalance will solve itself.

The implication of that is that high prices don’t last. In fact, a guy I’ve worked with for a couple of decades now – Madsen Pirie – likes to quote Thomas Sowell on the point. The cure for high prices is high prices. High prices shake out greater supply, the increase in supply lowers prices.

Do not, therefore, believe the idea that high prices will last off into the future. For they won’t.

With lithium, my favourite number is 2,850,000 billion tonnes. Yes, that’s near three million, billion, tonnes. That’s my calculation and is therefore wrong, but it’s within a couple of orders of magnitude of being right. The scientists have a general idea of the composition of the surface of the planet, each element this has a Clark Number. Times that by the weight of the lithosphere, and we get how much of that element is available.

No, no, of course we can’t get it all. Can even get the tiniest fraction of it. But the Tesla Master Plan 3 tells us we need 20 million tonnes of Li for the world’s supply of EVs. We need 20 million tonnes, we’ve millions of tonnes – no, we’re not going to run out. To put this less alarmingly, global lithium resources are put at 105 million tonnes, and that itself is a rise of 7 million tonnes from just the year before. We found near half of what we need in just the one year, that is. We’re really not going to run out.

Not only are we really not going to run out we’re going to have – in time, in time – a supply of whatever amount we need. Yes, prices will vary because prices do. But they’re never going to rise to come permanently high plateau. They’ll be a little above production cost in fact. A little above with variances, obviously but just a little above.

That’s the background that I insist upon.

Lithium isn’t particularly difficult to mine. There are salt brines out there, spodumene deposits, geothermal waters, a little more expensive lepidolite and mica deposits and so on. Yes, there can be gaps between how much is consumed this year and how much produced this year but because none of this is a particularly difficult mining operation prices are going to get out of what for a few years at most. As they did that few years back. And as they stopped being in only a few years. As they did in 2013 and as they stopped being a few years later.

Now, of course, it’s wholly possible to disagree with me on this. Sure, I know a bit about mining, and I was/am an expert in a particular very specific subset of it. But that subset doesn’t include lithium – I’m just perhaps better informed than most, that’s all. So, disagree by all means. But do understand where I’m coming from.

Ganfeng Lithium

I wrote about Ganfeng two years back – actually two years to the day by some coincidence. The share price at the time was $6.47. Today it’s $2.42. My read then?

“Therefore I’m bearish on Ganfeng. Not enough to recommend a short simply because I almost never do so recommend. But I’m not bull.”

Which seems to have worked.

Obviously, the question though is where now? And I can see that Ganfeng might do better than it is currently. Obviously, there could be one of those cyclical swings in lithium prices. I don’t think there will be, but that’s an opinion not a proof. They might get their costs down a bit and climb up out of their current losses. But I have a fairly dark feeling that their cost base is pretty much baked in.

But my big worry is that of two years back. During that boom in prices Ganfeng went out and bought assets. Assets that were, obviously enough, priced against that high lithium price at the time. This is going to be true of anything bought in the sector. Operating assets, prospecting licences, anything, they all go up in price when the production price rises.

This is leveraged by the system structure

The basic lithium set up

We don’t need to go through the whole of the lithium metal production cycle, nor really the battery production one. The economic issue here is the spodumene to battery chemicals cycle.

Yes, there are other sources – brines, geothermal and so on. But the thing that drives this part of the industry structure is the spod to carbonate part.

The typical product from a mine is a 6% lithium spodumene concentrate. Yes, there are variations, but that’s the standard that we need to think about. Mines tend to be of a certain size because deposits do too.

However, the processing of that concentrate into the actual lithium chemicals for battery making is a process with large economies of scale. Very large in fact, so much so that pretty much no mine does it themselves. But also no one processor can be fed by the output of just the one mine. The natural economic effect of this is that would be miners look for investment from processors in order to get the mine running. The processors look to finance mines in order to feed their processing plant.

At a time of rising prices this leads to something of a frenzy among the processors to establish their position as the pre-eminent one. Also, to ensure they’re financing enough new mines to feed their planned expansion of processing facilities.

Add in deliberately low costs of capital in China – part of the CCP’s build China program – and we can see what will happen.

This is also what did happen. Ganfeng bought into – and sometimes bought entirely – mine prospects. To the point that they’re now an integrated lithium supplier, from hole in the ground to battery chemicals. Great.

It’s just that some too many of those mine assets were bought into at the high prices of a few years back. Exactly the thing I worried about those two years ago.

Finances

As a Chinese company, we don’t get huge insight into the accounts, but this latest presentation is enough for us:

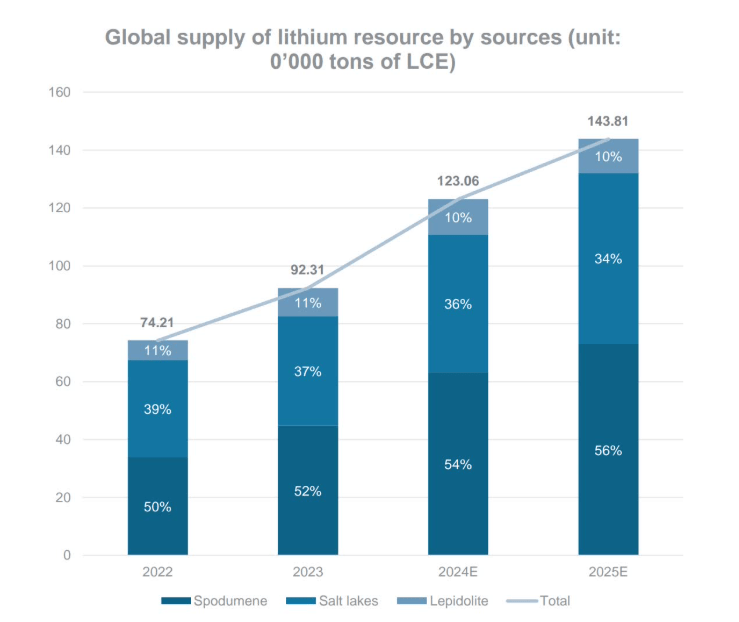

Lithium production (Ganfeng)

Well, not so much production as what is already listed as can be produced from. But we also have prices:

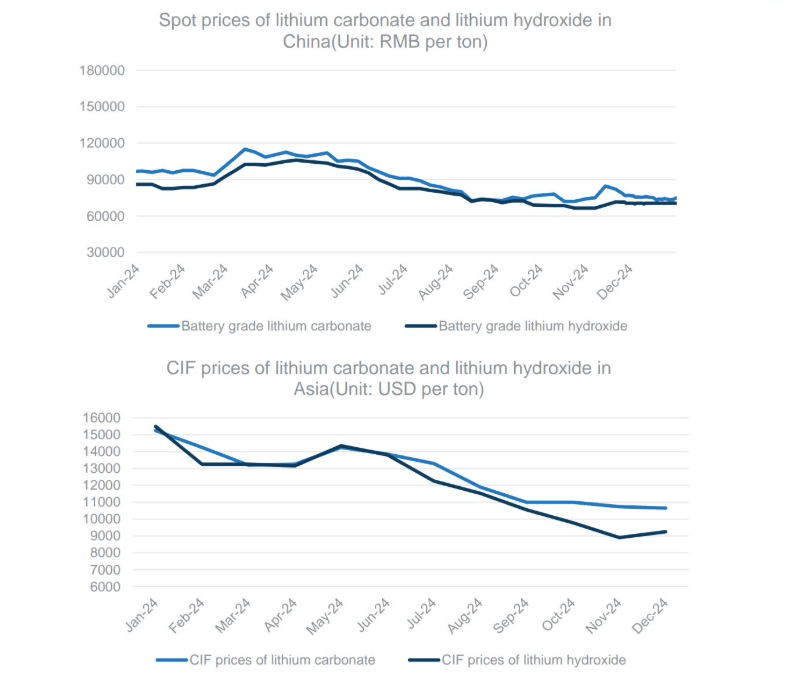

Lithium prices (Ganfeng)

Prices are going down. We really do not have a shortage of current production. In fact, we even have perfectly acceptable, capable of producing, mines on care and maintenance because it’s just not worth mining – like at Core Lithium.

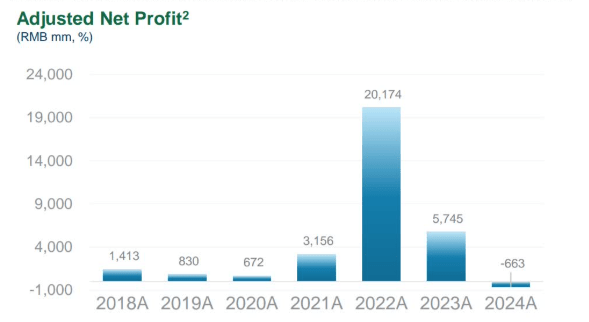

This has an effect on profits, obviously:

Ganfeng profits (Ganfeng)

Profits soared with the lithium price. They’re now negative – slightly. Because the lithium price has fallen as we all find out, there’s a lot of lithium about.

And, obviously, Ganfeng bought into lithium supplies when lithium was expensive.

So, what next?

If we were talking about a US company, then we’d want a lot more detail of the internal finances. With a Chinese champion like these we not only don’t need them, we’re not going to get them. Ganfeng isn’t going to go bust. Capital is cheap in China, and the CCP is going to make sure it is directed to those champions. That is just not something we need to worry about, at least not on anything like a likely investment timescale for us.

What we need to have is a view on the likely lithium price. If that goes up then so will Ganfeng’s profits and their stock price. If it doesn’t then, well, it won’t.

Which leads us to having to take that view. My view is that the lithium price isn’t going to bounce. Yes, I know, lots of people insisting it will. Demand is going to soar, and that just proves it. On the other hand, there’s a lot more lithium out there than most think. We have – as with Core – perfectly reasonable mines not producing right now. Price edges up a bit and they’ll come back.

My view is that the world not only has well, well, more than enough potential lithium it’s got enough nascent to extant production capacity to prevent – or at worst react quickly to – any uptick in demand.

Not that’s a view, an opinion. It’s not something I can prove. While I’ve been right in the past, a couple of times, on this that is no proof that I will be again.

Why am I wrong?

Sure, it could be true that demand for lithium soars, thus the price does. I would be wrong if it does – not the demand but the price. So, take my view as being counter to that risk.

My opinion

Ganfeng is indeed a major, global, integrated producer of lithium. They do it very well. As an industrial process, they’re great. Their profits, thus their stock price, to me depend upon the global price of lithium. As I don’t see that price rising in a major way off into the indeterminate future then I don’t see the stock price doing so either.

There’s another way to put this

Minor metals are subject to vast price swings. A new use arrives, prices soar, then we all find there’s a lot of that metal out there. New production comes online prices go back to sleep. The question is always how long are they going to go back to sleep for? My view on lithium? We’ve had our fun, and now it’s going to be boring.

So, to have investment fun we should be elsewhere. Lithium’s just so three years ago.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.